In today’s healthcare environment, understanding the role and significance of Personal Health Insurance is vital. Medical expenses continue to rise globally, making it increasingly important to secure a financial safety net for your health needs. This comprehensive guide explores what Personal Health Insurance is, its benefits, how it works, and whether it’s an essential part of your financial and health planning.

Key Takeaway

Investing in Personal Health Insurance provides not just financial security but also access to timely medical care and peace of mind. In an unpredictable world, this insurance acts as a safety net ensuring that your health does not become a financial burden.

Understanding Personal Health Insurance

Personal Health Insurance is a form of insurance policy that individuals purchase to cover their healthcare expenses. Unlike group or employer-provided insurance, personal health insurance is tailored specifically to the individual’s needs, offering flexibility and control over coverage. It acts as a financial safeguard against the potentially high costs associated with medical care, hospitalization, surgeries, and treatments.

What Is Personal Health Insurance?

At its core, Personal Health Insurance is a contract between you (the insured) and an insurance company (the insurer). You pay a fixed amount called a premium, either monthly, quarterly, or annually. In return, the insurer agrees to cover part or all of your healthcare expenses as defined in your policy. These expenses typically include hospital stays, doctor visits, surgeries, diagnostic tests, medicines, and sometimes outpatient services.

The main purpose is to reduce the financial burden on individuals when they face medical emergencies or ongoing health conditions. Healthcare costs are unpredictable and can be exorbitant; having personal health insurance helps in managing these costs without depleting savings or incurring debt.

How Does Personal Health Insurance Work?

The mechanism of personal health insurance involves several key components:

- Premium: The amount you pay regularly to keep your insurance active.

- Sum Insured: The maximum amount the insurer will pay for claims within the policy period.

- Deductible: The amount you pay out-of-pocket before the insurer starts covering expenses.

- Co-payment: A percentage of the cost you share with the insurer during claim settlement.

- Coverage: The specific medical treatments and services that the policy includes.

- Exclusions: Conditions or treatments not covered by the policy.

- Waiting Period: The time period before certain benefits or pre-existing conditions are covered.

When you receive medical treatment, you can either pay first and file a claim for reimbursement or use the cashless facility available in many policies, where the insurer directly settles the bills with the hospital.

Why Is Personal Health Insurance Important?

Medical treatments can quickly become expensive, especially for surgeries, chronic disease management, or emergency care. Without insurance, you bear the full financial impact, which can disrupt your finances drastically. Personal Health Insurance is important because:

- It protects you from unexpected, high medical bills.

- It enables timely access to healthcare services without financial hesitation.

- It provides peace of mind knowing that your health expenses are partially or fully covered.

- It encourages preventive care by covering health check-ups and screenings in some policies.

- It can cover a wide range of medical needs including inpatient and outpatient treatments.

Types of Coverage in Personal Health Insurance

When you purchase Personal Health Insurance, it is important to know the variety of coverage options available. These different types of coverage determine what medical expenses your policy will cover, how much protection you receive, and how flexible your plan is. Insurance providers design policies to cover a broad spectrum of healthcare needs, and understanding these coverage types allows you to select the right plan tailored to your health and financial situation.

Hospitalization Coverage

This is the fundamental and most common type of coverage in Personal Health Insurance policies. It covers expenses incurred during inpatient treatment at a hospital. The key components covered typically include:

- Room Rent and Boarding Charges: Costs for your hospital room, ICU stays, nursing, and other inpatient services.

- Doctor’s Fees: Charges for consultations, surgeries, and specialist visits during hospitalization.

- Surgical Expenses: Operating theater fees, surgeon charges, anesthesia, and related procedural costs.

- Medicines and Consumables: Medicines, blood, oxygen, and other consumables required during the hospital stay.

- Diagnostic Tests: Tests conducted during hospitalization like blood tests, X-rays, MRI, CT scans, etc.

Hospitalization coverage protects you from the substantial costs of serious illnesses, accidents, and surgeries that require admission to a hospital.

Pre-Hospitalization Coverage

Pre-hospitalization coverage reimburses or covers medical expenses incurred before hospital admission. Usually, it covers diagnostic tests, doctor consultations, and prescribed medicines for a specified period (often 30 to 60 days) prior to hospitalization.

This is important because many serious illnesses require tests or preliminary treatment before the patient is admitted to a hospital for further care.

Post-Hospitalization Coverage

Similar to pre-hospitalization, post-hospitalization coverage covers medical expenses after you are discharged from the hospital. This period typically ranges from 60 to 90 days after discharge, depending on the policy.

Post-hospitalization expenses may include follow-up doctor visits, medications, physiotherapy, and any other prescribed treatment necessary for recovery.

Daycare Procedures Coverage

Daycare procedures refer to medical treatments or surgeries that do not require 24-hour hospitalization. These include minor surgeries or therapies like chemotherapy, dialysis, cataract surgery, or endoscopy.

Since these procedures can be expensive, coverage under daycare procedures helps policyholders manage costs without requiring extended hospital stays.

Domiciliary Treatment Coverage

Domiciliary treatment coverage applies to medical treatments received at home when hospital admission is not possible or advisable due to patient condition or lack of hospital beds. Conditions like post-operative recovery or chronic illnesses may qualify.

This coverage is particularly useful for patients who need continuous medical supervision but cannot or prefer not to stay in the hospital.

Ambulance Charges Coverage

Many Personal Health Insurance plans cover ambulance charges incurred during emergencies. This includes transportation from home to hospital or between medical facilities.

This benefit ensures that you don’t have to worry about transportation costs in critical situations when timely medical help is crucial.

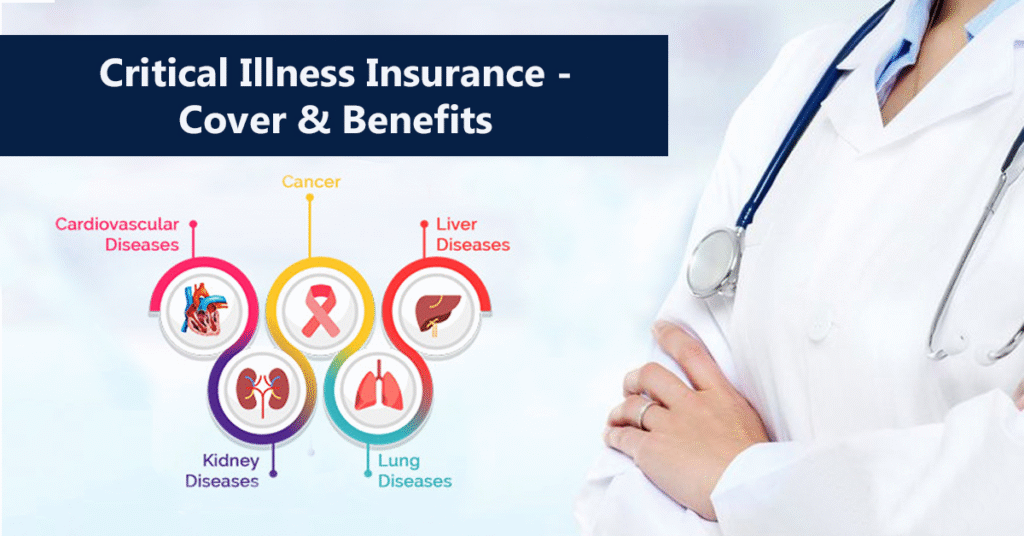

Critical Illness Coverage

Critical illness coverage can either be a standalone policy or an add-on rider to your basic health insurance. It offers a lump sum payment if you are diagnosed with a specified critical illness such as cancer, heart attack, stroke, kidney failure, or major organ transplant.

The lump sum can be used to cover treatment expenses, rehabilitation, or even non-medical costs like income loss during recovery.

Maternity and Newborn Coverage

Some Personal Health Insurance plans include maternity benefits that cover pregnancy-related expenses, including prenatal care, delivery charges, and postnatal care. This coverage often comes with waiting periods ranging from 9 months to 3 years.

Newborn coverage may also be included or available as an add-on, ensuring your baby’s healthcare costs are protected from birth.

Outpatient Department (OPD) Coverage

OPD coverage reimburses or covers expenses related to outpatient treatments such as doctor consultations, diagnostics, and minor procedures that do not require hospitalization.

This coverage is becoming popular as it helps manage routine medical costs and reduces the need for frequent hospital admissions.

Preventive Care Coverage

Some modern Personal Health Insurance plans include coverage for preventive health services such as annual health check-ups, vaccinations, screenings, and wellness programs.

Preventive care coverage encourages early detection and management of health issues, promoting long-term well-being.

Mental Health Coverage

Given the growing awareness around mental health, some insurers now include or offer riders for mental health treatment, including therapy sessions, counseling, and psychiatric medication.

This type of coverage is essential as mental health treatment costs can add up and are critical for overall health.

Wellness and Alternative Therapy Coverage

Certain policies cover alternative or complementary treatments such as physiotherapy, chiropractic care, acupuncture, or naturopathy, either as part of the base policy or as add-ons.

Such coverage supports holistic health management alongside conventional medical treatments.

Customizing Your Personal Health Insurance

One of the advantages of personal health insurance is the ability to choose add-ons or riders to enhance your policy. These might include:

- Critical illness cover: Provides a lump sum on diagnosis of specified critical illnesses.

- Maternity benefits: Covers pregnancy, delivery, and newborn care.

- Dental and vision care: Coverage for routine dental and eye care.

- Accident cover: Additional protection for accidental injuries.

- No claim bonus: Increased sum insured or premium discount if no claims are made during a policy year.

Who Should Consider Personal Health Insurance?

Personal health insurance is beneficial for:

- Self-employed individuals without employer coverage.

- Those whose employer-provided health plans are insufficient or limited.

- Individuals with specific health risks or family history of illnesses.

- Senior citizens who require specialized healthcare.

- Anyone who wants comprehensive coverage beyond government or employer schemes.

Factors Influencing the Cost of Personal Health Insurance

The premium and cost of personal health insurance depend on multiple factors such as:

- Age of the insured.

- Medical history and existing health conditions.

- Sum insured and coverage extent.

- Lifestyle factors like smoking, alcohol use.

- Geographic location and access to healthcare facilities.

- The insurer’s underwriting policies.

Choosing the Right Personal Health Insurance Policy

Choosing the right personal health insurance policy involves:

- Assessing your medical needs and budget.

- Comparing policies from multiple insurers.

- Checking claim settlement ratios and customer reviews.

- Understanding exclusions, waiting periods, and renewal terms.

- Ensuring the availability of cashless treatment facilities.

- Considering future needs like family coverage or chronic illness management.

Why Personal Health Insurance Matters

Healthcare costs have skyrocketed over the past decades due to advances in technology, inflation, and changes in health trends worldwide. Whether it’s an emergency surgery, chronic illness management, or even routine checkups, medical expenses can strain your finances without adequate coverage.

Personal Health Insurance acts as a safeguard against these financial shocks. It provides a means to manage your healthcare spending efficiently and avoid depleting your savings or taking on unmanageable debt during medical emergencies.

Moreover, having Personal Health Insurance ensures timely access to medical services. Without insurance, many delay or avoid necessary care due to costs, which can worsen health outcomes.

How Does Personal Health Insurance Work?

When you purchase Personal Health Insurance, you enter into a contract that specifies:

- The coverage limits (how much the insurer will pay)

- The premiums (how much you pay regularly)

- Deductibles and co-payments (your share of costs)

- Covered services (hospitalization, outpatient treatment, medications, etc.)

- Exclusions (what is not covered)

- Waiting periods (time before coverage starts for certain conditions)

Upon needing medical care, policyholders can use their insurance to pay for services either by submitting claims post-treatment or by using cashless facilities offered by many insurers at network hospitals. The insurer reimburses or directly pays the hospital, reducing out-of-pocket expenses.

The details of how claims work, the extent of coverage, and the network of hospitals available depend heavily on the insurance provider and plan chosen.

Types of Personal Health Insurance Plans

There are various types of Personal Health Insurance plans designed to suit different needs:

- Indemnity Plans: These reimburse medical expenses after treatment.

- Managed Care Plans: These limit coverage to specific networks of doctors and hospitals.

- Fixed Benefit Plans: These pay fixed amounts for certain treatments regardless of actual costs.

- Critical Illness Plans: Cover major illnesses like cancer or heart disease.

- Maternity Plans: Focus on childbirth and related healthcare.

- Senior Citizen Health Plans: Tailored for older adults with specific health risks.

Understanding your needs is crucial before selecting a plan.

Benefits of Personal Health Insurance

- Financial Security: The primary benefit is protection from high medical costs.

- Access to Quality Healthcare: Insurance policies often provide access to a wide network of hospitals.

- Cashless Treatment: Many insurers offer cashless hospitalization at network hospitals.

- Tax Benefits: Premiums paid for Personal Health Insurance can often be claimed as tax deductions.

- Peace of Mind: Knowing you have coverage helps reduce stress about potential health issues.

- Coverage for Pre-existing Conditions: Some policies cover existing health problems after waiting periods.

- Additional Benefits: Such as wellness programs, preventive care, and outpatient treatments.

Do You Really Need Personal Health Insurance?

Whether you need Personal Health Insurance depends on many factors such as:

- Your current health status

- Family medical history

- Financial stability

- Access to employer-sponsored health plans

- Risk tolerance for medical emergencies

If you are young, healthy, and have access to group insurance, you might feel less urgency. However, personal insurance fills the gaps in employer or government plans. It offers continuous protection if you change jobs, retire, or become self-employed.

For families and individuals with chronic health conditions, Personal Health Insurance is often indispensable. It also plays a key role for those seeking comprehensive and personalized healthcare solutions.

How to Choose the Right Personal Health Insurance Plan

| Factor | What to Look For | Why It Matters |

|---|---|---|

| Coverage Amount (Sum Insured) | Adequate coverage based on your lifestyle, age, and location | Ensures sufficient financial support during medical emergencies |

| Premium Cost | Affordable premium for the benefits offered | Helps maintain the policy long-term without financial strain |

| Hospital Network | Wide network of trusted and nearby hospitals offering cashless facilities | Enables hassle-free treatment and fast claim processing |

| Pre and Post-Hospitalization | Minimum 30-60 days before and 60-90 days after hospitalization | Covers related diagnostic tests, consultations, and follow-up care |

| Daycare Procedures | Coverage for treatments that don’t need 24-hour hospitalization (e.g., dialysis, cataract surgery) | Reduces out-of-pocket costs for common short procedures |

| Waiting Periods | Shorter waiting periods for pre-existing diseases and maternity cover | Faster access to complete coverage, especially for known health issues |

| Co-Payment Clause | Lower or no co-payment | Reduces the portion of medical bills you pay from your pocket |

| Claim Settlement Ratio (CSR) | Look for insurers with CSR above 90% | Indicates the insurer’s reliability and ease of claim approval |

| Cashless Hospitalization | Included in policy with a broad hospital network | Simplifies admission and payment during emergencies |

| Policy Renewability | Lifetime renewability | Ensures continued coverage in old age when health issues are more likely |

| Coverage for Pre-existing Diseases | Available with a reasonable waiting period | Important for individuals with known chronic illnesses |

| Ambulance Charges | Should be included up to a sufficient limit | Covers emergency transport without extra cost |

| Maternity and Newborn Cover | Optional add-on or built-in if planning a family | Provides financial support for pregnancy and child care expenses |

| Critical Illness Cover | Option to add or buy separately | Offers lump-sum financial assistance for life-threatening conditions |

| OPD & Preventive Health Check-ups | Included or available as add-ons | Helps in managing day-to-day and long-term health proactively |

Selecting the right Personal Health Insurance plan can be daunting. Here are some critical steps:

- Assess Your Healthcare Needs: Consider your age, health, lifestyle, and family medical history.

- Compare Plans: Look at premiums, deductibles, coverage limits, and exclusions.

- Check Network Hospitals: Ensure your preferred hospitals and doctors are in-network.

- Review Policy Terms: Understand waiting periods, renewal terms, and claim procedures.

- Read Customer Reviews: Check insurer reputation and customer service.

- Evaluate Additional Benefits: Look for preventive care, wellness programs, and value-added services.

- Seek Professional Advice: Consult insurance brokers or financial advisors if needed.

Common Misconceptions About Personal Health Insurance

- It’s too expensive: While some plans can be costly, many affordable options exist tailored for different budgets.

- Young people don’t need it: Health emergencies can happen at any age.

- Government health schemes are enough: They may not cover all treatments or provide comprehensive benefits.

- It’s complicated to claim: Many insurers have simplified digital claims processes.

- Pre-existing conditions are never covered: Some insurers offer coverage after waiting periods.

Also Read: What Is Car Insurance Online and How Does It Work?

Conclusion

Personal Health Insurance is a vital aspect of modern financial and health planning. It offers financial protection, access to quality healthcare, and peace of mind. While individual needs vary, having personal health insurance generally strengthens your ability to handle medical expenses without jeopardizing your financial stability.

By evaluating your health risks, understanding policy details, and selecting the right plan, you can secure your health and that of your loved ones.

FAQs

What is covered under personal health insurance?

Coverage varies but generally includes hospitalization, surgeries, outpatient treatments, diagnostics, and sometimes preventive care.

Is personal health insurance mandatory?

No, but it is highly recommended to avoid high medical costs and ensure access to healthcare.

How does cashless treatment work?

In cashless treatment, the insurer pays the hospital directly for eligible expenses, reducing out-of-pocket costs.

Can I have personal health insurance along with employer insurance?

Yes, this can enhance your coverage and fill any gaps.

Are there tax benefits with personal health insurance?

In many countries, premiums paid for personal health insurance are tax-deductible up to a certain limit.

What are waiting periods in personal health insurance?

Waiting periods are the initial time frames during which certain conditions or treatments are not covered.

How do I file a claim?

Claims can be filed online or offline by submitting medical bills and documents as per the insurer’s process.