Buying a home is one of the most significant financial decisions many people will ever make. The process can be exciting but also overwhelming, especially when it comes to securing financing. A critical step in this journey is obtaining a home loan preapproval, a process that not only clarifies your borrowing power but also strengthens your position in the real estate market. But what exactly is a home loan preapproval, and why does it matter so much for prospective homebuyers? This article will explore the ins and outs of home loan preapproval, its benefits, the process, and why it is often considered an essential step before you start house hunting.

Key Takeaways

- A home loan preapproval is a formal assessment of your ability to borrow, involving document verification and credit checks.

- It helps you understand your budget and shop for homes realistically.

- Sellers view preapproved buyers as serious and financially capable, giving you an edge.

- The process can reveal financial issues early, allowing you to address them.

- Preapproval can expedite the final mortgage approval and closing process.

- It is generally valid for 60 to 90 days and subject to re-verification.

- Maintaining good financial habits after preapproval is crucial for securing the loan.

Understanding Home Loan Preapproval

A home loan preapproval is a formal process in which a lender evaluates a potential borrower’s financial health to determine the amount they are eligible to borrow to purchase a home. This is a crucial step for prospective homebuyers because it sets realistic expectations about what they can afford and strengthens their credibility in the eyes of sellers.

Unlike a simple prequalification, which is generally a quick and informal estimate based on unverified financial information, a home loan preapproval requires the borrower to submit actual financial documents for verification. The lender then analyzes these documents along with a credit check to provide a conditional approval for a mortgage loan.

Key Components of Home Loan Preapproval

To understand home loan preapproval fully, it’s important to know what factors lenders consider and how the process works:

Financial Documentation

Borrowers are asked to provide documents that demonstrate their ability to repay the loan. This typically includes:

- Recent pay stubs or proof of income

- Tax returns for the past two years

- Bank statements showing savings and assets

- Proof of employment

- Identification documents

- Details of existing debts and financial obligations

The lender reviews these documents to verify income stability and assess financial health.

Credit Check

One of the most important parts of the preapproval process is a hard inquiry into the borrower’s credit report. This check provides insight into the borrower’s credit history, including payment timeliness, outstanding debts, credit utilization, and any derogatory marks. A strong credit score generally improves chances of approval and can lead to better interest rates.

Debt-to-Income Ratio (DTI)

Lenders calculate the debt-to-income ratio to determine if the borrower has sufficient income to handle new mortgage payments in addition to existing debt obligations. The DTI ratio is the percentage of monthly income that goes toward debt payments. Most lenders prefer a DTI below a certain threshold (often around 43%), but requirements can vary.

Loan Amount and Terms

Based on the above factors, lenders decide on a maximum loan amount they can extend to the borrower and may specify tentative loan terms such as interest rates, repayment period, and type of loan.

How the Home Loan Preapproval Helps Borrowers

Navigating the home-buying process can be complex and stressful. For most people, purchasing a home is the largest financial commitment they will ever make. One tool that greatly simplifies this journey and empowers buyers is the home loan preapproval. Obtaining a home loan preapproval before you begin your house hunt offers several crucial benefits that can save time, reduce stress, and improve your chances of securing the home you want under favorable terms.

Provides Clarity on Your Budget

One of the biggest challenges in buying a home is understanding exactly how much you can afford. Many buyers overestimate or underestimate their borrowing capacity. A home loan preapproval provides a clear, realistic picture of the loan amount you qualify for based on your verified income, creditworthiness, debts, and other financial factors.

With this information, you can focus your home search on properties within your price range. This prevents disappointment from falling in love with homes that are out of reach financially and helps you avoid wasting time on unaffordable options.

Strengthens Your Position in a Competitive Market

In a seller’s market where multiple buyers compete for limited properties, sellers look for offers backed by serious, financially capable buyers. A home loan preapproval letter from a reputable lender shows sellers that you have already been vetted and approved for financing up to a certain amount.

This demonstrates that your offer is credible and that you can close the deal without financing delays or uncertainty. As a result, preapproved buyers are often prioritized over those who haven’t yet secured loan approval, which can be a decisive advantage when sellers receive multiple offers.

Accelerates the Loan Approval and Closing Process

The mortgage process typically involves extensive paperwork, verifications, and underwriting, which can take weeks. When you obtain a home loan preapproval, much of this financial vetting is completed upfront. The lender has already reviewed your documents, checked your credit, and determined your eligibility.

So, once you find a home and make an offer, the final mortgage approval can proceed faster because the lender doesn’t have to start from scratch. This acceleration benefits both you and the seller by shortening the time to close, making the transaction smoother and less stressful.

Helps Identify and Resolve Credit or Financial Issues Early

During the preapproval process, lenders perform a thorough review of your financial situation, including credit reports and income verification. This early check can uncover potential problems, such as low credit scores, unresolved debts, or insufficient income documentation, which might hinder your loan approval.

Knowing about these issues ahead of time gives you an opportunity to address them—whether by paying down debt, correcting credit report errors, or saving for a larger down payment—before you start seriously looking at homes. This proactive approach improves your chances of final loan approval and better loan terms.

Provides Insight Into Loan Options and Terms

A home loan preapproval also educates you about what kinds of loans you qualify for, such as fixed-rate or adjustable-rate mortgages, conventional or government-backed loans, and the likely interest rates and down payment requirements.

This information helps you make informed choices tailored to your financial goals and circumstances. You can compare different loan products and understand the long-term impact on your monthly payments and total loan costs.

Encourages Financial Discipline and Plannin

The process of gathering documents and going through preapproval encourages borrowers to get their finances in order. It highlights the importance of steady income, manageable debt levels, and saving for down payments and closing costs.

Having a home loan preapproval in hand also motivates borrowers to avoid new debt or major financial changes during the home buying process, which could jeopardize their loan approval.

Builds Confidence and Peace of Mind

Knowing that a lender has conditionally approved you for a mortgage can provide significant psychological comfort during a potentially stressful time. This confidence allows you to negotiate assertively, act quickly when you find the right property, and avoid the anxiety of uncertainty about financing.

What Happens After Preapproval?

A home loan preapproval is generally valid for a limited period, often between 60 and 90 days. After this, if you haven’t purchased a home, you may need to update your financial information for an extension or a new preapproval.

Once you find a home and make an offer, the lender moves to the full underwriting process, which includes an appraisal of the property, more detailed financial verification, and final loan approval. While preapproval is a strong indicator of loan eligibility, it is not a guarantee; changes in your financial situation or issues with the property can affect final approval.

Differences Between Preapproval and Prequalification

| Aspect | Prequalification | Preapproval |

|---|---|---|

| Definition | An initial estimate of how much you might borrow based on self-reported information. | A formal evaluation involving verification of financial documents and credit check. |

| Process | Quick and informal, often online or over the phone. | Detailed and formal, requiring submission of documentation. |

| Credit Check | Usually no credit check or a soft inquiry. | Hard credit inquiry performed. |

| Documentation Required | Minimal or none; based on self-reported info. | Requires income proof, tax returns, bank statements, etc. |

| Reliability | Less reliable; an estimate only. | More reliable; conditional commitment from lender. |

| Validity Period | Generally informal with no fixed validity. | Typically valid for 60 to 90 days. |

| Impact on Loan Approval | Does not guarantee loan approval. | Strong indicator and often a prerequisite for loan approval. |

It’s worth distinguishing home loan preapproval from prequalification. Prequalification is an informal estimate of borrowing capacity often done online or over the phone, based on self-reported information without document verification or credit checks. Preapproval, on the other hand, involves actual document review and credit inquiries, making it a more reliable and formal indication of loan eligibility.

The Importance of Home Loan Preapproval

When embarking on the journey to purchase a home, understanding your financial standing and borrowing capacity is essential. A home loan preapproval is a powerful tool that serves this purpose by providing a lender’s conditional approval of your loan application based on your financial information. It goes beyond simple estimation and gives both buyers and sellers confidence in the home financing process.

The importance of obtaining a home loan preapproval lies in the many advantages it offers throughout the home-buying process — from helping buyers budget realistically to providing a competitive edge in negotiations, and from speeding up loan processing to revealing potential financial issues early. Let’s explore these reasons in detail.

Establishes a Clear Financial Framework

One of the fundamental reasons why a home loan preapproval matters is that it establishes a clear and realistic financial framework for homebuyers. The preapproval process involves thorough verification of income, credit history, debts, and other financial metrics, which enables the lender to provide a specific loan amount you qualify for.

This clarity allows buyers to shop for homes within an affordable price range, preventing them from wasting time on properties that are outside their financial reach. It also helps avoid the emotional rollercoaster of falling in love with a home only to realize later that financing isn’t possible.

Builds Credibility and Trust with Sellers

In real estate transactions, credibility is key. Sellers want to deal with buyers who are financially capable of completing the purchase without delays or complications. A home loan preapproval letter signals to sellers and real estate agents that you have been vetted by a lender and are a serious buyer.

This can make your offer stand out, especially in competitive markets where multiple buyers vie for the same property. Sellers are more likely to accept offers backed by preapproval because it reduces the risk of the sale falling through due to financing issues.

Accelerates the Mortgage Approval Process

Another critical importance of the home loan preapproval is that it jumpstarts the mortgage approval process. Since much of the documentation and financial verification is completed during preapproval, the lender is already familiar with your financial background.

Once you select a property and submit a formal loan application, the lender can move more quickly through underwriting and approval steps. This can reduce the time it takes to close on your home, which benefits both buyers and sellers by making the transaction more efficient.

Identifies Potential Financial Barriers Early

The preapproval process often acts as an early warning system. By conducting a thorough review of your financial situation, the lender may identify issues that could hinder your ability to secure a loan, such as low credit scores, outstanding debts, or insufficient documentation.

Identifying these barriers early gives you a valuable opportunity to take corrective action — whether that means paying down debt, disputing errors on your credit report, or gathering additional documents — before you get serious about buying a home. This proactive approach can save time and frustration later.

Improves Loan Terms and Interest Rates

Buyers who come to the table with a home loan preapproval often have an advantage in negotiating better loan terms and interest rates. Lenders view preapproved buyers as lower-risk borrowers because they have already passed initial screening.

This can translate into more favorable interest rates, lower fees, or better loan options, which can save significant amounts of money over the life of the loan. Additionally, it gives you leverage to shop around and compare offers from different lenders with preapproval letters in hand.

Provides Confidence and Peace of Mind

Buying a home is a significant emotional and financial undertaking. Having a home loan preapproval provides peace of mind by assuring you that you are financially prepared to move forward. This confidence allows you to approach the home search and negotiation stages with greater certainty and less anxiety.

Knowing that a lender has conditionally approved your loan empowers you to make informed decisions and act decisively when you find the right home.

Facilitates Better Financial Planning

The process of obtaining a home loan preapproval also encourages better financial planning. It prompts you to organize your financial documents, assess your income and debts, and understand your credit profile in detail.

This preparation helps you set realistic expectations for down payments, monthly mortgage payments, closing costs, and other expenses involved in home buying. It also helps you avoid surprises that could disrupt your financial stability.

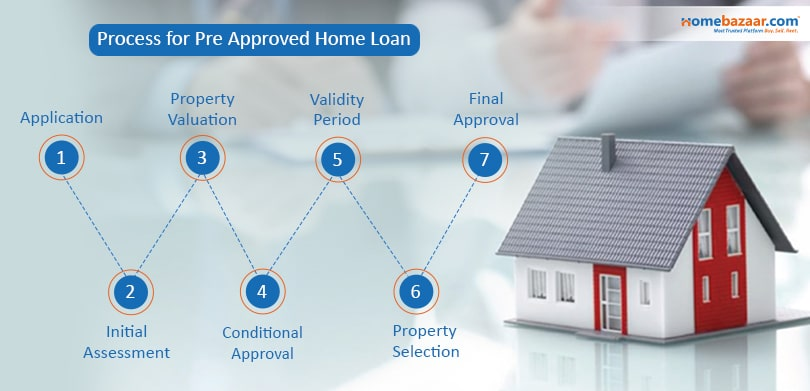

The Home Loan Preapproval Process

Obtaining a home loan preapproval typically involves several key steps:

- Financial Documentation Submission: You provide the lender with documents such as pay stubs, tax returns, bank statements, and identification.

- Credit Check: The lender runs a credit check to assess your credit score and credit history.

- Income and Employment Verification: The lender verifies your income and employment status.

- Debt and Expense Review: They evaluate your existing debts and monthly expenses to calculate your debt-to-income ratio.

- Preapproval Decision: Based on this information, the lender issues a preapproval letter that states the loan amount you qualify for, valid for a specific period (usually 60 to 90 days).

Benefits Beyond the Home Search

Beyond helping you narrow down your home search and strengthening your offer, a home loan preapproval can also help you:

- Set realistic expectations regarding monthly mortgage payments.

- Understand your borrowing capacity relative to your financial goals.

- Plan your finances, including savings for down payments and closing costs.

- Build confidence when interacting with sellers and real estate agents.

Common Mistakes to Avoid

Even after obtaining a home loan preapproval, it’s crucial to maintain good financial habits, such as avoiding new debts or major purchases, which could jeopardize your approval. Additionally, not all preapprovals are created equal—some lenders may offer soft preapprovals that aren’t as binding, so it’s essential to understand the terms clearly.

Also Read: What Does a Loan Agent Really Do?

Conclusion

Obtaining a home loan preapproval is a strategic step for anyone serious about buying a home. It empowers you with a clear understanding of your borrowing capacity, strengthens your negotiating position, and streamlines the mortgage process. While it does not guarantee loan approval, it puts you in a stronger position to act swiftly and confidently when you find the right property. Given the competitive nature of the housing market, securing a home loan preapproval should be considered a vital part of your home buying plan.

FAQs

What is the difference between home loan preapproval and prequalification?

Prequalification is an initial estimate based on self-reported information, whereas preapproval is a formal process involving document verification and a conditional loan commitment.

How long does a home loan preapproval last?

Typically, a home loan preapproval is valid for 60 to 90 days, but this can vary by lender.

Can I get preapproved by multiple lenders?

Yes, you can seek preapprovals from multiple lenders to compare offers and find the best terms.

Does applying for a home loan preapproval affect my credit score?

Yes, a hard inquiry is usually made during preapproval, which can have a slight temporary impact on your credit score.

What documents do I need for home loan preapproval?

Common documents include pay stubs, tax returns, bank statements, identification, and credit history.

Can a preapproval guarantee that I will get the loan?

No, it is conditional and subject to further verification and appraisal of the property you intend to buy.

Is home loan preapproval required to buy a house?

It’s not legally required, but it is highly recommended to increase your chances of successful purchase and negotiation.