In today’s fast-paced digital world, businesses are increasingly seeking quick and efficient ways to secure funding. One of the most popular methods is obtaining a business loan online. This modern approach to financing has transformed how businesses manage cash flow, invest in growth, and navigate challenges. But what exactly is a business loan online, and how does it work? This article delves deep into the concept, exploring every aspect of online business loans, their benefits, the application process, types, eligibility, and much more.

Key Takeaways

- Business loan online allows borrowing money through digital platforms without physical bank visits.

- The application process is fast, with minimal paperwork and quick approval.

- Various loan types are available, including term loans, lines of credit, and invoice financing.

- Eligibility criteria differ but generally focus on business age, revenue, and credit scores.

- Benefits include convenience, speed, and access to flexible financing.

- Risks involve higher interest rates and the need to avoid scams by verifying lenders.

- Future trends will likely make online business loans even more accessible and tailored.

Understanding Business Loans Online

In the evolving landscape of business financing, the concept of a business loan online has gained significant traction. It represents a modern, technology-driven approach to accessing capital that contrasts sharply with traditional lending methods. To truly understand what a business loan online entails, it’s important to break down its components, mechanisms, and implications for businesses of all sizes.

What Exactly Is a Business Loan Online?

At its core, a business loan online is a financial product designed to provide working capital, investment funds, or operational cash flow to businesses through internet-based platforms. Unlike traditional loans, which typically require in-person visits to banks or lending institutions, online business loans leverage digital technologies to simplify, speed up, and automate the loan application and approval process.

The loan funds can be used for various business needs, including:

- Purchasing inventory or equipment

- Expanding operations or facilities

- Hiring new employees or contractors

- Managing day-to-day cash flow gaps

- Marketing and promotional campaigns

- Refinancing existing debts

The online aspect means the entire process—from application and document submission to approval and fund disbursement—occurs through secure websites or mobile apps.

The Digital Transformation of Business Financing

The rise of online business loans reflects a broader digital transformation within financial services. Traditional lending often involved lengthy paperwork, credit committee meetings, physical visits, and slow decision-making. This inefficiency often hampered small and medium-sized enterprises (SMEs) and startups, which require agility and fast access to capital.

Online lending platforms have revolutionized this by:

- Automating underwriting: Advanced algorithms and artificial intelligence analyze financial data swiftly.

- Streamlining documentation: Digital document uploads and integrations with bank accounts reduce manual input.

- Providing instant quotes: Businesses can receive customized loan offers based on real-time data.

- Enabling remote management: Loan tracking, repayment, and communication happen online.

As a result, the online model democratizes access to capital, opening doors for many businesses that previously struggled with traditional banks.

How Do Online Lenders Assess Your Business?

Unlike traditional banks that often rely heavily on credit history and collateral, many online lenders use alternative data points to evaluate loan applications. While creditworthiness remains important, online lenders may also consider:

- Bank transaction data: Frequent deposits, consistent cash flow, and overall revenue patterns.

- Business performance metrics: Sales growth, profit margins, and operational stability.

- Online presence: Website traffic, social media activity, and digital sales channels.

- Industry risk factors: Lenders assess how your business fits within the risk profile of your industry.

- Personal credit: Especially for small businesses and startups, the owner’s personal credit score often plays a key role.

This broader view allows lenders to better understand the true financial health and future potential of your business.

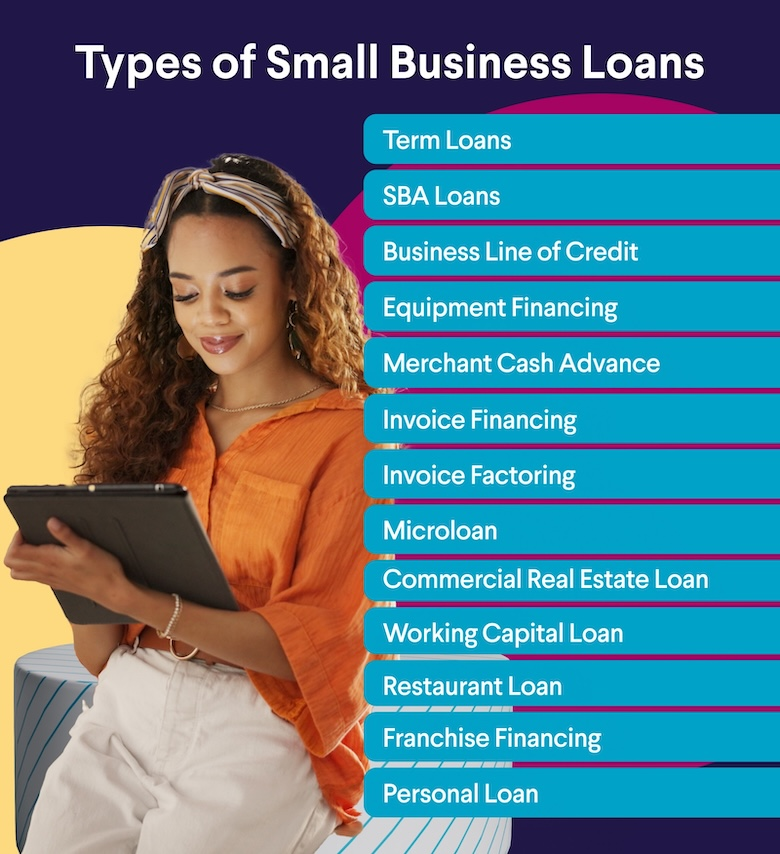

Types of Online Business Loans and Their Uses

When exploring business loan online options, it’s important to understand the various loan types that lenders offer. Each has distinct features tailored to specific business needs.

- Term Loans: These provide a lump sum amount repaid over a fixed period with interest. They are ideal for one-time investments like equipment purchases or facility expansion.

- Business Lines of Credit: A revolving credit line that businesses can draw from as needed. Interest is charged only on the amount drawn, making it flexible for managing cash flow fluctuations.

- Invoice Financing: This loan allows businesses to borrow against outstanding invoices. It’s useful for companies facing delayed payments from customers.

- Merchant Cash Advances: Here, lenders provide an upfront amount based on future sales, repaid through a percentage of daily credit card receipts. This suits businesses with steady sales but irregular cash flow.

- Equipment Financing: Specifically for purchasing business equipment, this loan often uses the equipment itself as collateral.

- SBA Loans Online: Some online lenders facilitate access to loans backed by the Small Business Administration, offering lower rates and longer repayment terms.

Understanding which loan type fits your business needs can dramatically impact your financial health and repayment success.

The Application Process: Step-by-Step

Applying for a business loan online is typically more straightforward than traditional loans but still requires careful preparation.

- Research and Select Lenders: Not all online lenders serve the same businesses. Choose lenders with good reputations and loan products suited to your needs.

- Prepare Your Documents: Commonly requested documents include business registration papers, tax returns, bank statements, financial statements, and personal identification.

- Complete the Online Application: Fill out detailed forms on the lender’s platform, providing accurate information about your business and loan requirements.

- Submit Documentation: Upload digital copies of your documents. Some platforms use bank account linking to automatically retrieve financial data.

- Wait for Approval: Many lenders provide decisions within 24 to 48 hours using automated underwriting.

- Review Loan Offer: Carefully read the terms, interest rates, fees, and repayment schedules before accepting.

- Receive Funds: Upon acceptance, funds are electronically transferred to your business bank account, often within a day or two.

- Repay Loan: Manage your repayments through the lender’s online portal or automatic deductions.

Key Advantages of Business Loans Online

- Speed: Many lenders process applications and disburse funds faster than traditional banks.

- Convenience: The entire process is accessible remotely, saving time and travel.

- Accessibility: Businesses with shorter operating histories or lower credit scores may find it easier to qualify.

- Transparency: Online lenders often provide upfront, clear terms with no hidden surprises.

- Flexibility: Multiple loan products allow tailored financing solutions.

Challenges and Considerations

While online business loans offer many benefits, it’s essential to be mindful of:

- Higher Interest Rates: Especially for unsecured loans or riskier businesses, rates may be higher than bank loans.

- Shorter Terms: Some loans require quick repayment, which can strain cash flow.

- Scam Risks: The rise in online lending means increased risk of fraudulent lenders. Always verify legitimacy.

- Impact on Credit: Borrowing and repayment behavior affect business and personal credit profiles.

A business loan online is a financing option provided by lenders through digital platforms, allowing businesses to borrow money for various purposes. Unlike traditional loans, which require physical visits to banks or financial institutions, online business loans offer the convenience of applying, processing, and managing loans entirely via the internet.

This type of loan caters to startups, small businesses, and established companies looking for capital infusion without the cumbersome paperwork or long waiting periods associated with conventional loans. The entire process is streamlined, leveraging technology, automation, and digital verification methods.

Why Choose a Business Loan Online?

The appeal of a business loan online lies in its speed, accessibility, and simplicity. Business owners can apply anytime, anywhere, without the need for in-person meetings or lengthy documentation. Lenders use automated systems to assess creditworthiness, speeding up approvals and disbursements.

Some of the key reasons businesses opt for online loans include:

- Fast approval and disbursal: Many online lenders can approve loans within 24 to 48 hours.

- Minimal documentation: Digital applications require fewer documents compared to traditional loans.

- Convenience: Apply from your office or home without visiting a bank.

- Flexible loan amounts and repayment terms: Various options suit different business needs.

- Access for businesses with less-than-perfect credit: Some lenders specialize in high-risk loans.

How Does a Business Loan Online Work?

The process of obtaining a business loan online is straightforward but involves several critical steps. Understanding this process helps businesses prepare better and improve their chances of approval.

Application Submission

The first step is submitting an online application through the lender’s website or mobile app. Applicants need to provide essential information such as:

- Business details (name, registration, type)

- Financial information (revenue, expenses, bank statements)

- Personal information of the business owner(s)

- Loan amount and purpose

The application may require uploading scanned copies of necessary documents, but many online lenders also use bank integration tools to pull financial data automatically.

Loan Pre-Approval and Verification

Once the application is submitted, the lender’s system performs an initial evaluation. This includes:

- Credit score check (business and/or personal)

- Review of financial statements and cash flow

- Assessment of business history and operations

Verification may be partly automated or supplemented with manual review by loan officers. Some lenders might conduct a quick video call or request additional information for clarity.

Loan Offer and Terms

After approval, the lender presents the business with a loan offer detailing:

- Loan amount approved

- Interest rate or fee structure

- Repayment schedule (monthly, weekly, or daily)

- Loan tenure

- Any applicable penalties or prepayment options

Businesses can review and accept or negotiate terms online.

Loan Disbursement

Upon agreement, the funds are transferred electronically to the business’s bank account. This is usually done within a day or two, depending on the lender’s processing time.

Repayment

Businesses repay the loan as per the agreed schedule, with repayments debited automatically or paid manually. Online lenders often provide dashboards or apps to track payments, outstanding balances, and upcoming due dates.

Types of Business Loans Available Online

Online lending platforms offer various types of business loans to suit different requirements. Each loan type serves specific purposes and comes with unique features:

- Term Loans: Traditional loans with fixed repayment terms, usually ranging from 1 to 5 years. Ideal for purchasing equipment, inventory, or expansion.

- Business Lines of Credit: Flexible credit amounts that businesses can draw from as needed. Interest is paid only on the amount used.

- Invoice Financing: Allows businesses to borrow against outstanding invoices to improve cash flow.

- Merchant Cash Advances: Advances based on future sales, repaid through a percentage of daily credit card transactions.

- Equipment Financing: Loans specifically for purchasing machinery or equipment.

- SBA Loans Online: Some platforms facilitate access to Small Business Administration-backed loans with favorable terms.

- Short-Term Loans: Loans with shorter durations and faster repayment schedules, often used to cover immediate expenses.

Eligibility Criteria for Business Loan Online

The eligibility requirements for a business loan online vary by lender, but common criteria include:

- Minimum business age (often 6 months to 1 year)

- Minimum annual revenue (varies widely)

- Credit score thresholds (personal and business)

- Valid business registration and licenses

- Proof of income and cash flow stability

- Bank statements and financial records

Many online lenders are more flexible than traditional banks, allowing startups or businesses with lower credit scores to qualify, although the interest rates may be higher.

Benefits of Business Loan Online

| Benefit | Description |

|---|---|

| Speedy Approval & Disbursal | Online loans often get approved within 24-48 hours, with funds disbursed quickly to your account. |

| Convenience | Apply anytime and anywhere without visiting a bank branch, saving time and travel. |

| Minimal Documentation | Reduced paperwork compared to traditional loans, often requiring only digital uploads. |

| Flexible Loan Options | Various loan types (term loans, lines of credit, invoice financing) tailored to business needs. |

| Accessibility | Easier qualification criteria, helping startups and businesses with less-than-perfect credit. |

| Transparent Terms | Online platforms provide clear terms and fees upfront, reducing hidden costs or surprises. |

| Automated Process | Use of technology and AI speeds up credit assessment and decision-making. |

| Easy Repayment Tracking | Online dashboards and apps allow businesses to monitor loan status and upcoming payments. |

| Improved Cash Flow Management | Quick access to funds helps businesses manage day-to-day expenses and seize growth opportunities. |

| No Collateral Often Required | Many online loans are unsecured, reducing risk to business assets. |

| Enhanced Customer Support | Many lenders offer 24/7 online support and real-time communication channels. |

| Access to Competitive Rates | Ability to compare multiple lenders online to find the best interest rates and terms. |

The benefits of choosing a business loan online are numerous, making it a preferred choice for many entrepreneurs:

- Speed and Efficiency: Online loans can be approved and disbursed quickly, enabling businesses to seize opportunities or address urgent needs.

- Accessibility: Even businesses in remote areas can access funds without traveling to a bank.

- Less Paperwork: The digital process reduces hassle and saves time.

- Transparent Terms: Online platforms often provide clear details and tools to compare offers.

- Variety of Loan Products: Diverse options tailor financing to specific business needs.

- Improved Cash Flow Management: Access to working capital helps businesses stabilize operations.

Potential Drawbacks and Risks

While a business loan online offers many advantages, businesses should be aware of potential downsides:

- Higher Interest Rates: Some online lenders charge higher rates, especially for high-risk borrowers.

- Shorter Repayment Terms: Fast approvals often come with quicker payback periods.

- Risk of Scams: Unscrupulous lenders exist; businesses must research and verify legitimacy.

- Impact on Credit: Late or missed payments can negatively affect credit scores.

- Hidden Fees: It’s vital to read loan agreements carefully to avoid unexpected charges.

Tips to Secure a Business Loan Online Successfully

To maximize the chances of obtaining a business loan online with favorable terms, consider the following tips:

- Maintain a strong credit score and resolve any issues before applying.

- Prepare accurate and up-to-date financial documents.

- Choose lenders specializing in your industry or business size.

- Compare multiple loan offers and understand the terms thoroughly.

- Clearly state the loan purpose and how it will benefit your business.

- Ensure your business is legally registered and compliant with regulations.

- Use business banking accounts with consistent transactions.

The Future of Business Loans Online

With advancements in technology, the future of business loan online platforms looks promising. Artificial intelligence, blockchain, and enhanced data analytics will improve credit assessments and offer even more personalized loan products. Additionally, greater integration with business software will simplify bookkeeping, loan monitoring, and repayment processes.

Also Read: What Are Car Loan Terms and Why Do They Matter?

Conclusion

A business loan online represents a revolutionary shift in business financing, combining convenience, speed, and accessibility with the flexibility needed by today’s entrepreneurs. Whether you need capital to expand your operations, manage cash flow, or invest in new equipment, online business loans provide an efficient alternative to traditional lending.

Understanding how these loans work, the types available, eligibility requirements, and the associated benefits and risks is crucial to making an informed decision. While online loans are not without challenges, the right preparation and lender choice can significantly improve your chances of securing funds that drive your business forward.

FAQs

What is a business loan online?

A business loan online is a financing option where businesses apply and receive funds through digital platforms without visiting a bank physically.

How long does it take to get approved for a business loan online?

Approval times vary, but many online lenders offer decisions within 24 to 48 hours, with funds disbursed shortly after approval.

Can startups get a business loan online?

Yes, many online lenders cater to startups, although requirements may include a minimum operating period and proof of income.

What are typical interest rates for online business loans?

Rates vary widely depending on creditworthiness, loan type, and lender, ranging from single-digit percentages to over 30% APR in some cases.

Is collateral required for business loans online?

Some loans are unsecured, but others, especially larger amounts, may require collateral such as equipment or property.

How is the repayment schedule determined?

Repayment schedules depend on loan terms agreed upon at approval and can be monthly, weekly, or daily.

Are business loan online applications safe?

Reputable lenders use secure websites and encryption to protect applicant information. Always verify the lender’s credibility before applying